We are often asked by new and potential clients if it possible to get forecasted returns with ETFmatic. It’s important to start any answer to this question by saying that any and all forward estimates carry with them a whole range of assumptions and should always be taken with a large pinch of salt. What we aim to provide is a range of possible returns, however the actual returns that you experience could be far different.

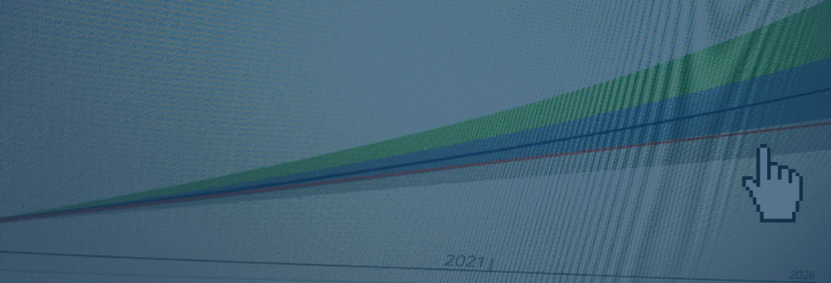

With the disclaimers highlighted we then direct clients to the tool we have under the performance tab in the app where clients can enter their initial and ongoing contributions. This tool uses a monte carlo simulation (a random walk methodology) that takes an estimated return along with standard deviation numbers to arrive at a range of possible outcomes. In the past we have used data from our data provider along with a Black Litterman model to arrive at the expected return and standard deviations. As the asset allocations and ETFs in the portfolios evolved however, we have now updated this forecasting tool with a new methodology.

We’ve arrived at the portfolio returns and volatility by using actual ETF data going back as far as we could gather data for. Using the oldest Nominal Government Bond ETFs, Inflation-Linked Bond ETFs along with the MSCI All Countries World Index ETF we replicated the same asset allocation as our model portfolios. Using this historical data we arrived at the historical returns and volatilities of our 21 static asset allocations. From 100% Fixed Income to 100% equities.

Every method used to arrive at robust numbers has some flaw embedded in it. Our method replicates our asset allocations relatively accurately (using the same asset allocations and using actual ETF return data), however suffers from the flaw of ETFs only being around for roughly a decade. This means our historical numbers are not based on very long-term data. We will continue to update these numbers wherever possible, therefore providing more market cycles and asset class returns underlying these numbers.

This update has resulted in our future estimated projections being pushed slightly higher for our asset allocations This is quite evident in our EUR and GBP models. For example, our 100% EUR and GBP equity allocations produce returns of 8.86% and 10.51% p.a., which are high by historical standards. We’ll provide the same caveat again and say that actual investment returns may vary greatly from any calculations. In order to arrive at our forecasted fan chart we used our historical calculated returns and volatilities in our monte carlo simulation. The monte carlo, using the random walk methodology, then produces the range of possible outcomes given our two inputs.

We wish we could predict the future accurately for our clients. It would make our and your life far easier. We certainly don’t pretend that any forward estimates we provide to you are to be taken as gospel. However, what we try and do is provide our clients with relatively robust calculations and methodology and using standard financial modelling in order to arrive at a range of possible returns that could be possibly be achieved in the real world. We think this update improves upon our last method and hopefully provides a more accurate forward estimate.